Blog + News

2022 Federal Budget Details – Continued Spending With Limited Tax Measures

On April 7, 2022, the Government of Canada released the 2022 Federal Budget. Like the 2021 budget, which we blogged about here, the government is continuing to spend tremendous amounts of money with deficits that have no end in sight. For 2022-2023, the federal deficit is projected to be $52.8B and $39.9B for 2023-2024. For a small country like Canada, these deficit amounts are tremendously high but admittedly lower than the $113B expected for the 2021-2022 year and over $300B for the 2020-2021 year. With strong performances by the oil and gas sector and high inflation, tax revenues were higher than expected thus giving the government incentives to spend more. Time will tell how Canada deals with its deficit management, inflationary pressures, and labor shortages.

With significant spending promises made by the Liberal Party during the 2021 federal election along with economic challenges mostly presented by COVID issues, many professionals have been very concerned about how taxation policies might be impacted to ensure Canada has sufficient funds to provide for its necessary spending. With the recent NDP-Liberal Party “coalition”, there has been even more concern especially if one has previously reviewed the 2021 election policy platforms of both federal parties. There have been many prognosticators – including us – who have made predictions on how tax rates, capital gains inclusion rates and the possible introduction of new taxes might arise. The 2022 Budget, for now, answers some of those questions.

This year’s budget contained some interesting tax measures that our firm’s audience will be most interested in. For those not interested in reading the entire blog, below is an executive summary of the tax measures relevant to our clients and friends:

EXECUTIVE SUMMARY

- No personal tax rate increases – notwithstanding the NDP party’s 2021 election policy platform that promised to raise personal tax rates for the “wealthy” by an additional 2%, there are no direct personal tax rate increases in the budget.

- No corporate tax rate increases (except for certain financial institutions as described below) – there were no general corporate tax rate increases in the budget.

- No capital gains inclusion rate increases – despite significant concern and predictions by many – including us – that the capital gains inclusion rate would increase from its current rate of 50%, there are no capital gains inclusion rate increases in the budget.

- No introduction of a new “wealth tax” – despite numerous recommendations made by way of papers and articles released by left-wing “think-tanks” over the last few years, there are no new wealth taxes included in the 2022 federal budget.

- No amendments to the principal residence exemption – while the budget did introduce an “anti-flipping” tax (more on this below), there are no proposed amendments to the principal residence exemption despite numerous concerns that the exemption might be changed.

- Bill C-208 – Another Consultation – the government is proposing yet another consultation on how to deal with the inter-generational transfer issue facing family businesses. Frustrating.

- Ban on Foreign Investment in Canadian Housing – the budget is proposing to impose a ban on “foreign money” being used to acquire Canadian housing. The proposal is sparse in detail and has more questions than answers.

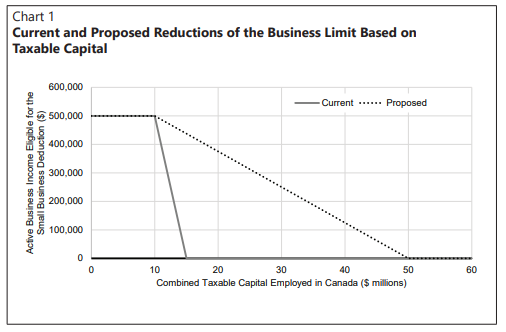

- Increasing Taxable Capital Threshold for Small Business Tax Rate – Good news for small businesses. The Budget proposes that, effective for taxation years that begin on or after April 7, 2022, the new small business tax rate phase out range will be between $10 million to $50 million of taxable capital (rather than between $10 million to $15 million currently). The more gradual pace of the small business limit grind should reduce disincentives for businesses to grow beyond $10 million of capital.

- Deferring Tax Using Foreign Entities – the Budget contains a two-prong approach to require certain corporations to be subject to the current refundable tax regime currently imposed on Canadian Controlled Private Corporations.

-

- Substantive CCPCs – the Budget and accompanying Notice of Ways and Means Motion introduces a new type of corporation, the “Substantive CCPC”. Essentially, any private corporation that is not a CCPC but is de facto controlled by Canadian residents will be subject to the refundable Part I and Part IV tax regimes.

- Modification of the taxation of Foreign Accrual Property Income (“FAPI”) – The Budget proposes alterations to the taxation of FAPI. The stated intent is to effectively tax FAPI earned by CCPCs or Substantive CCPCs at an upfront rate of 52.63% (inclusive of foreign tax paid). The Budget appears to also propose to fix the integration of FAPI such that the net tax on a fully distributed basis is equal to 52.63% through a combination of CDA inclusions, restriction of additions to the general rate income pool (“GRIP”) for FAPI and potentially altering the surplus definitions. The high-level commentary leaves more questions than answers and we anxiously await draft legislation to be able to understand the mechanisms that will attempt to accomplish these Budget goals.

- Residential Property Flipping Rule – the government intends to impose a rule that any profits from the disposition of residential real estate – including rental properties – that occurs less than 12 months from its acquisition date will be deemed to be business profits and not capital gains (thus excluding the disposition from being treated as a principal residence eligible for the related exemption) subject to certain “life event” exclusions. We believe this new proposal is littered with issues and not necessary to curb the abuse that it is intending to stop.

- Elimination of Flow-Through Shares for Oil, Gas and Coal Activities – the government strikes a blow against oil & gas and coal companies who seek financing through flow-through share issuances by eliminating the “flow-through share regime”.

- New 30% Critical Minerals Exploration Tax Credit – the Budget provides an opportunity for investors in critical minerals to realize a 30% investor tax credit under the proposed Critical Minerals Exploration Tax Credit.

- Expansion of the GAAR to Tax Attributes – the Budget proposes to overturn the Wild case by legislating that a “tax benefit” now includes increase or preservation of tax attributes. As a result, GAAR can now apply to abusive tax avoidance transactions where only tax attributes (e.g., PUC, CDA, losses, etc.) are created or preserved. This may not be a bad amendment from a policy perspective, but we are disappointed that the government proposes to implement this retroactively so that historical transactions are also subject to this amendment to the extent they haven’t yet been issued a GAAR notice of determination before the Budget date.

- A Commitment to Create a New Minimum Tax Regime for “High Earners” – the government announced that in the 2022 fall economic and fiscal update, it will release details on a proposed new minimum tax. No details have been released to date. What was noteworthy was the misleading statistics cited by the government, which adds nothing substantive to the real conversation needed in this country. Stay tuned….as the government is already indicating the economic and fiscal update will have important tax measures.

- Additional Taxes on Large Financial Institutions – the Budget proposes to introduce two additional significant taxes on affected financial institutions. We believe there are significant concerns with these additional taxes that we hope the Government has carefully thought through.

- Employee Ownership Trusts – the Budget announces that it will create a new dedicated type of trust – the Employee Ownership Trust – to support and encourage employee ownership of a business. Consultations will continue and no further details were released.

- Government to Review the SR&ED Program – The SR&ED Program will be reviewed to ensure that it targets research, development, and the development of intellectual property beneficial to Canada. The proposed review will also consider the application of a “patent box” regime.

- More Money for the Canada Revenue Agency (“CRA”) – The government proposes to, once again, allocate significantly more resources to the Canada Revenue Agency.

- GST/HST on Assignment Sales – Budget 2022 proposes to amend the Excise Tax Act to make all assignment sales in respect of newly constructed or substantially renovated residential housing taxable for GST/HST purposes.

- New ‘Boutique Tax Credits’ – Budget 2022 delivers a bounty of “boutique tax credits”. A little something for everyone it seems.

ANALYSIS

Bill C-208 – Further Consultation

Bill C-208 has an interesting and notorious history. For good background, have a listen to our firm’s TaxBreak’s podcast numbers 020 and 021 that can be accessed here. The short story is that Bill C-208 that received Royal Assent last June 2021 was an imperfect bill that dealt with the long-standing problem of the Income Tax Act not providing for tax efficient transfers of family businesses to the next generation as compared to arm’s length transfers. This problem has existed since 1985. In 2017, the government asked for submissions on how to deal with this long-standing issue. Credible organizations and people provided good submissions on the topic. Unfortunately, the government did not materially move forward other than to continually assert that they were interested in trying to come up with an efficient solution to the problem.

When Bill C-208 (a private members bill) unexpectedly passed, it was obvious that the government was surprised with the passing of the imperfect bill. It released a press release in July 2021 promising to release draft legislation soon, but it has not yet done so. In the budget materials, the government is now proposing to commence anotherconsultation asking for submissions from stakeholders no later than June 17, 2022. After the consultation, the government states that it will release draft legislation in the fall of this year.

Overall, the above announcement is frustrating. Another consultation? How many consultations and “listening tours” (there was a “listening tour” on this topic in 2018 as well) does the government need? Can they simply not review previous submissions and reach out to those stakeholders to address any concerns? Disappointing. Meanwhile, Bill C-208 is effective, and the Department of Finance has previously indicated that it will remain effective until draft legislation is released and ultimately passed.

Ban on Foreign Investment in Canadian Housing

The federal budget documents contain the following comment:

There is concern that foreign investment, property flipping and speculation, and illegal activity are driving up the cost of housing in Canada.

….

For years, foreign money has been coming into Canada to buy residential real estate. This has fueled concerns about the impact on costs in cities like Vancouver and Toronto and worries about Canadians being priced out of the housing market in cities and towns across the country.

To make sure that housing is owned by Canadians instead of foreign investors, Budget 2022 announces the government’s intention to propose restrictions that would prohibit foreign commercial enterprises and people who are not Canadian citizens or permanent residents from acquiring non-recreational, residential property in Canada for a period of two years.

While the above ban is not a tax measure, we could not resist the urge to comment on this proposed measure. It is devoid of detail. Some of the obvious questions are:

- What exactly is a “foreign commercial enterprise”?

- Will this proposal expedite the need for “beneficial registries” for corporations in every provincial jurisdiction?

- How will the federal government work with the provincial governments to implement?

- What exactly is a non-recreational, residential property? Will there be a clear and objective definition of that type of property? Or will foreigners simply be able to assert that the property they are acquiring is a recreational property?

- From when will this measure take place? In other words, two years from which date?

- What impact will this have on the Canadian housing market? Many Canadians’ net worth is materially tied up in their principal residence. Will this proposal – along with inevitable interest rate increases that are coming – negatively impact Canadians’ value in their residences in a significant fashion? Also, there appears to be no consideration about local market conditions. Not all real estate markets across Canada are overheated.

We crave details.

Increasing Taxable Capital Threshold for Small Business Tax Rate

There is some good news for small businesses across Canada. The Budget is proposing to significantly increase the range of taxable capital before the small business deduction limit is reduced to nil. Under existing tax rules, a CCPC’s ability to access the small business tax rate of 9% (federally) is limited to the first $500,000 of active business income earned in Canada for the associated corporate group. This $500,000 limit is reduced on a straight-line basis when combined taxable capital employed in Canada by the associated group is between $10 million and $15 million. Because this grind in the limit is so steep between $10 to $15 million, businesses have for years complained about this being a large disincentive for growth beyond $10 million capital.

We are glad that the government has finally decided to address this. The Budget proposes that, effective for taxation years that begin on or after April 7, 2022, the new small business tax rate phase out range will be between $10 million to $50 million as illustrated in the graph below. To be clear, the small business limit will still begin phasing out at $10 million, but the grind down is now at a much more gradual pace until the $500,000 business income limit is completely gone by the $50 million taxable capital mark.

It is important to remember that the grind to the small business limit is still the greater of the taxable capital grind above and the “passive income” grind which begins when a corporation has $50,000 of adjusted aggregate investment income and the small business limit is reduced to $nil when the passive income reaches $150,000. The Budget contained no changes to the “passive income” grind reducing the small business deduction.

Substantive CCPCs

The Budget has made it clear that the Department of Finance believes that many private Canadian resident corporations that are not CCPCs should be subject to the same taxation regime as CCPCs. The Budget sets out to eliminate any tax deferral for corporations that have been manipulated such that they are no longer CCPCs and are not subject to the “anti-deferral” refundable Part I tax regime. Earlier this year, the government first targeted these structures with draft legislation that proposes such transactions (transactions that convert a CCPC to a non-CCPC) to be “notifiable transactions” to be reported to CRA.

The Budget introduces the “Substantive CCPC”. Unlike most of the other tax measures proposed by the Budget, a legislative definition was included in the Notice of Ways and Means Motion to amend the Act. Specifically, subsection 248(1) of the Income Tax Act is proposed to now include:

Substantive CCPC means a private corporation (other than a Canadian-controlled private corporation) that at any time in a taxation year

- is controlled, directly or indirectly in any manner whatever, by one or more Canadian resident individuals, or

- would, if each share of the capital stock of a corporation that is owned by a Canadian resident individual were owned by a particular individual, be controlled by the particular individual.

The Act will also contain a specific anti-avoidance provision with respect to Substantive CCPCs that will deem a corporation that would otherwise not be a Substantive CCPC to be a Substantive CCPC where one of the purposes of any transaction or series of transaction was to cause the corporation to not be a substantive CCPC. This is extremely broad legislation and makes it clear that the intent is to capture all planning related to causing a corporation to be a non-CCPC to defer taxation.

The affront to the Canadian tax system stated in the Budget is that corporations that are factually resident in Canada but are formed or continued (to use the Budget language, “manipulated”) to a foreign jurisdiction would no longer be CCPCs and as such would not be subject to the refundable Part I tax regime that CCPCs are subject to. The above new definition will also catch any corporation that loses its CCPC status due to a foreign entity having any right to acquire a CCPC, which legitimately occurs in many sale transactions.

To be fair, these proposed budgetary changes are based on sound policy. Corporations should not be able to manipulate their status to avoid the Part I refundable tax regime that CCPCs are subject to. It should be pointed out, however, that the new definition of Substantive CCPC contains no language that restricts its application to corporations that have been “manipulated” to no longer being CCPCs. The blanket definition applies in all cases regardless of intent or whether a corporation has lost its status in a transaction with no tax motivation. Even the Budget itself states that the Act already contains provisions that would allow the Government to challenge CCPC status manipulation, but nonetheless, the government is choosing to add additional provisions to capture such scenarios.

Additionally, there are further revisions and potential additions to the Act that have not yet been drafted. These appear to include:

- a one-year extension of the normal reassessment period for Substantive CCPCs for any assessment or reassessment of Part IV tax arising from a corporation being assessed or reassessed a dividend refund;

- investment income earned by a Substantive CCPC would be added to the corporation’s low-rate income pool;

- provisions to include Substantive CCPCs in the ambit of refundable Part I tax: and

- any other modifications necessary to give effect to the Substantive CCPC proposals.

Modification of the Taxation of Foreign Accrual Property Income

Budget 2022 also includes proposed measures to eliminate tax deferrals on Foreign Accrual Property Income (“FAPI”) earned in foreign corporations owned by CCPCs or Substantive CCPCs. The stated goal is to subject FAPI earned by controlled foreign affiliates (“CFAs”) to an immediate tax rate of 52.63% (Canadian and foreign tax inclusive) and to introduce mechanisms to apply integration to FAPI earned by CFAs held by CCPCs and Substantive CCPCs to have fully distributed FAPI to a resident individual be subject to the aforementioned 52.63%.

Prior to the Budget, FAPI earned by a CFA held by a CCPC would only be subject to Canadian tax if the foreign tax paid by the CFA on its FAPI was less than 25%. This was accomplished by providing the CCPC a deduction for foreign accrual tax (“FAT”) equal to the foreign tax paid multiplied by the relevant tax factor (“RTF”), which for corporations was 4. In the view of the Department of Finance, this provided an opportunity for tax deferral as CCPCs could transfer property that would earn passive income to a foreign corporation, or otherwise use a foreign corporation to invest in passive income producing property.

For example, a CCPC earning investment income (excluding dividends) would be subject to tax on its investment income at a rate of about 50%, with 30.33% of the investment income being refunded upon the payment of sufficient dividends. If the same income was earned by a CFA of a CCPC in a jurisdiction with a foreign tax rate of 25% (which includes many US states), no Canadian tax would result due to the FAT deduction (25% x 4 = 100% deduction). Thus, the result is a tax deferral of about 50% of the tax that a CCPC would have been subject to. The income could then be repatriated to the CCPC as a dividend with minimal or no Canadian tax as the CCPC should be entitled to deduct the amount of the foreign tax multiplied by the RTF (i.e., 4) minus one plus the amount of withholding tax multiplied by the RTF minus one (with respect to dividends paid out of taxable surplus).

Additionally, the amount of the deduction was added to the general rate income pool (“GRIP”) which effectively provides a preferential tax rate on dividends paid out of GRIP. It should be noted that, generally, on a fully distributed basis the tax integration of FAPI did not work particularly well often resulting in an overall tax rate upwards of 60% on a fully distributed basis in some cases. The main issue that the Budget is seeking to address is the tax deferral that can be realized.

To address and remove the deferral opportunity of CCPCs with CFAs earning FAPI, the Budget proposes to reduce the RTF to 1.9, the same RTF provided to individuals. This drastically reduces the FAT deductions available to CCPCs and thereby increases the amount of FAPI subject to additional Part I tax. To address tax integration, the Budget proposes to amend the definition of capital dividend account (“CDA”) to include, among other things, the amount repatriated to the CCPC by the CFA to the extent such earnings were subject to a tax rate of 52.63%. It would be quite the challenge to find any jurisdiction that imposes a corporate tax rate this large. The Budget also intends to include in CDA:

- the amount of an inter-corporate dividend deduction claimed with respect to a dividend paid out of hybrid surplus less the amount of withholding tax paid with respect to the dividend, and

- the amount of a withholding tax deduction claimed less the withholding tax paid in respect of repatriations of taxable surplus

The Budget also proposes to remove the additions to GRIP for amounts that would have been previously included, namely the deductions for the foreign tax and withholding tax paid by the CFA. This is presumably to assist with the intention to provide tax integration with respect to FAPI, however integration at a tax rate lower than 52.63% would be much preferred.

It is important to note that no draft legislation was released with the Budget on these measures. This is a substantial change to the taxation of FAPI earned by CCPCs and there are many unknowns as to how the integration will be implemented. It is likely a pipe dream for the integration to work perfectly, but it remains to be seen how closely the actual integration will be to the stated goal of 52.63%.

A few questions we have with respect to the new FAPI regime are:

- How will the refundable portion of Part I tax paid by the CCPC on its, now increased FAPI be treated?

- Are there any cases where non-eligible refundable dividend tax on hand cannot be recovered?

- Will the definition of hybrid surplus be amended to include a sale of underlying property that is not currently included in hybrid surplus (e.g., rental properties)? If something of this nature is not included, then it is likely that the integration goal of the Budget will not be met.

It is easy to understand the rationale for the inclusion of these measures, but without draft legislation it is impossible to assess the impact of these FAPI changes. It is safe to assume that the perfect integration goal will not be met, but how far off the stated goal and in what direction will need to wait until the legislation is released. Furthermore, any potential unintended consequences of these proposals will need to be identified upon the release of the draft legislation.

These changes will result in taxpayers with foreign affiliates that have FAPI to revisit their corporate structure, particularly if they were relying on 25% or greater foreign tax to negate any Canadian FAPI considerations.

“Residential Property Flipping Rule”

The Budget documents contain the following comments:

Property flipping involves purchasing real estate with the intention of reselling the property in a short period of time to realize a profit. Profits from flipping properties are fully taxable as business income, meaning they are not eligible for the 50-per-cent capital gains inclusion rate or the Principal Residence Exemption.

The Government is concerned that certain individuals engaged in flipping residential real estate are not properly reporting their profits as business income. Instead, these individuals may be improperly reporting their profits as capital gains and, in some cases, claiming the Principal Residence Exemption.

Budget 2022 proposes to introduce a new deeming rule to ensure profits from flipping residential real estate are always subject to full taxation. Specifically, profits arising from dispositions of residential property (including a rental property) that was owned for less than 12 months would be deemed to be business income.

The new deeming rule would not apply if the disposition of property is in relation to at least one of the life events listed below:

Death: a disposition due to, or in anticipation of, the death of the taxpayer or a related person.

Household addition: a disposition due to, or in anticipation of, a related person joining the taxpayer’s household or the taxpayer joining a related person’s household (e.g., birth of a child, adoption, care of an elderly parent).

Separation: a disposition due to the breakdown of a marriage or common-law partnership, where the taxpayer has been living separate and apart from their spouse or common-law partner because of a breakdown in the relationship for a period of at least 90 days.

Personal safety: a disposition due to a threat to the personal safety of the taxpayer or a related person, such as the threat of domestic violence.

Disability or illness: a disposition due to a taxpayer or a related person suffering from a serious disability or illness.

Employment change: a disposition for the taxpayer or their spouse or common-law partner to work at a new location or due to an involuntary termination of employment. In the case of work at a new location, the taxpayer’s new home must be at least 40 kilometres closer to the new work location.

Insolvency: a disposition due to insolvency or to avoid insolvency (i.e., due to an accumulation of debts).

Involuntary disposition: a disposition against someone’s will, for example, due to, expropriation or the destruction or condemnation of the taxpayer’s residence due to a natural or man-made disaster.

Where the new deeming rule applies, the Principal Residence Exemption would not be available.

Where the new deeming rule does not apply because of a life event listed above or because the property was owned for 12 months or more, it would remain a question of fact whether profits from the disposition are taxed as business income.

The measure would apply in respect of residential properties sold on or after January 1, 2023.

No detailed draft legislation was released in the accompanying Notice of Ways and Means Motion. However, the Budget documents further promise to consult with Canadians on the forthcoming draft legislation.

The proposals raise numerous questions and issues such as:

- Doesn’t the Income Tax Act already contain the legislative tools to curb “property flipping” and improper principal residence exemption claims? All dispositions of property are already required to be disclosed and reported. Under existing law, it is a question of fact as to whether a property disposition is on account of capital or income so someone who is buying properties to flip are already tax as if they are earning business income.

- To arbitrarily put a 12-month holding test will likely drive other unintended behaviour such as encouraging the disposition of property in month 13 from the date of acquisition. But even then, the existing provisions of the Income Tax Act can still provide that such a disposition is on account of income thus capturing mischievous misreporting.

- Why 12 months? Why not six months? 24 months? 36 months?

- Since 2016, any principal residence exemption claim must be explicitly reported and disclosed in personal tax reporting thus enabling the Canada Revenue Agency the ability to easily audit such claims.

- How will the “life event” exclusions listed above be policed by the Canada Revenue Agency? For example, what kind of evidence will need to be provided to prove that a disposition was necessary within the 12 months of acquisition due to a threat of personal safety? Or household addition (will one need to show house floor plans to prove that they couldn’t squeeze in another family member? Who will be the judge of that?)

In our view, this proposal is not necessary and will lead to additional administration for the Canada Revenue Agency. Instead, more enforcement action by the Canada Revenue Agency using existing legislative and administrative tools should be done to curb any abuse.

Elimination of the Flow-Through Share Regime for Oil, Gas and Coal

Certain corporations in the resource sector have long relied upon the issuance of flow-through shares to support the financing of exploration and project development activities. Junior resource corporations often have difficulty raising capital to finance their exploration and development activities. Moreover, many are in a non-taxable position and do not need to deduct their resource expenses. The flow-through share mechanism allows the issuer corporation to transfer the resource expenses to the investor. A junior resource corporation benefits greatly from flow-through share financing.

The flow-through share program provides tax incentives to investors who acquire flow-through shares by allowing:

- deductions for resource expenses renounced by eligible corporations; and,

- investment tax credits for individuals (excluding trusts) on resource expenses in the mining sector that qualify as flow-through mining expenditures.

These deductions can provide a deduction to the holder of the flow-through shares a 100% deduction of the renounced expenses for Canadian Exploration Expenses (CEE) or a 30% declining balance deduction for Canadian Development Expenses (CDE).

Consistent with the government’s messaging and policy initiatives around the oil and gas and the coal mining industry, Budget 2022 strikes another blow against corporations seeking to promote the development of our fossil fuel resources by proposing the elimination of the issuance of flow-through shares for corporations involved in oil & gas exploration and development and coal mining. This will effectively eliminate the flow-through share regime for oil, gas, and coal activities by no longer allowing oil, gas and coal exploration or development expenditures to be renounced to a flow-through share investor.

The Budget proposes that this change would apply to expenditures renounced under flow-through share agreements entered after March 31, 2023.

New 30% Critical Minerals Exploration Tax Credit

As electric vehicles (EV’s) become more and more popular, the demand for the critical minerals required to produce EV batteries has increased exponentially. Canada is fortunate to hold a wealth of mineral deposits critical to the development of EV batteries and permanent magnets and minerals necessary in the production and processing of advanced materials, clean technology, or semi-conductors.

Mining is, however, extremely capital intensive and companies involved in the exploration and development of these critical minerals must seek creative means of financing their activities which can often include the issuance of flow-through shares to investors. Currently, the Mineral Exploration Tax Credit (METC) provides an additional income tax benefit for individuals who invest in mining flow-through shares, which augments the tax benefits associated with the deductions that are flowed through. The METC is equal to 15 per cent of specified mineral exploration expenses incurred in Canada and renounced to flow-through share investors. The METC facilitates the raising of equity to fund exploration by enabling companies to issue shares at a premium.

This Budget proposes to introduce a new 30-per-cent Critical Mineral Exploration Tax Credit (CMETC) for specified minerals. The specified minerals that would be eligible for the CMETC are copper, nickel, lithium, cobalt, graphite, rare earth elements, scandium, titanium, gallium, vanadium, tellurium, magnesium, zinc, platinum group metals and uranium. These minerals are used in the production of EV batteries and other green energy infrastructure.

It is important to note that this does not provide for a “double-dip” credit opportunity as those investments that will benefit from the METC will not also be eligible for the CMETC.

For exploration expenses to be eligible for the CMETC, the exploration entity will be required to certify that the renounced expenses were incurred in the process of exploration and development of specified critical minerals. If the entity cannot demonstrate that there is a reasonable expectation that the minerals targeted by the exploration are primarily specified minerals, then the related exploration expenditures would not be eligible for the CMETC. Any credit provided for ineligible expenditures would be recovered from the flow-through share investor that received the credit.

It is interesting to note that, prior to Budget 2022, corporations engaged in the exploration and development of certain critical minerals in Canada (such as lithium) could not issue flow-through shares for financing purposes. With the introduction of these proposed rules, issuance of flow-through shares will now be available to companies seeking to exploit critical minerals in Canada.

It is also interesting to contrast the approach that has been taken by the government in addressing flow-through share issues for the mining of minerals deemed to be critical to green-energy development and the taxation of flow-through shares issued in the fossil fuel and coal sectors (see above).

The CMETC would apply to expenditures renounced under eligible flow-through share agreements entered into after April 7, 2022, and on or before March 31, 2027.

Expansion of the GAAR to Tax Attributes

The general anti-avoidance rule (“GAAR”) refers to section 245 of the Act which was first introduced into law by Parliament in 1988. Recognizing that it was impossible to legislate away all possible inappropriate tax avoidance planning, the GAAR gave the CRA broad powers to redetermine tax consequences of transactions where the resulting tax benefits represented a misuse or abuse of the relevant provisions of the Act. Over the years, a large body of case law has developed around when the GAAR should or should not apply.

The Budget proposes a change to the GAAR legislation to overturn case law that has ruled that the GAAR cannot apply to a transaction that merely results in an increase in a tax attribute that had not yet been utilized to reduce taxes (note, the case law suggested that GAAR may apply when the tax attribute was used to realize the benefit).

In order for for the GAAR to apply there must be a “tax benefit” resulting from a transaction or series of transactions. The term “tax benefit” is defined in subsection 245(1) of the Act and it refers to a reduction, avoidance, or deferral of tax (or increase in amount of tax refund). The Federal Court of Appeal in 1245989 Alberta Ltd (Wild), 2018 FCA 114, was decided on a matter whereby an individual taxpayer took advantage of the paid-up capital (PUC) averaging rule to create a class of shares that had both ‘soft’ tax cost (i.e., adjusted cost base created by gains fully sheltered by lifetime capital gain exemption) and high PUC. The existence of this PUC in the shares would permit a future strip of corporate assets without the specific anti-surplus-stripping avoidance rule in subsection 84.1(1) from applying. While the Tax Court found that the planning misused the PUC averaging mechanism of the Act to artificially inflate PUC, the Federal Court concluded that the GAAR could not apply because no corporate retained earnings had in fact been distributed. While the increased PUC created the potential for a tax-free strip of corporate retained earnings, that potential had, to date, not been realized. However, the court also noted the entitlement of the Minister to reassess the taxpayer when the taxpayer eventually removes the corporation’s corporate surplus as a tax-free return of capital. This would require the CRA to continuously monitor the taxpayer to assess GAAR when the PUC was used.

This concept was adopted by the Courts in subsequent cases. For example, in Gladwin Realty Corporation v. Canada, 2020 FCA 142, an increase in the capital dividend account (CDA) was found to not give to rise to a tax benefit until a capital dividend was paid out of that account.

The Government was not amused. Understandably so. Imagine the bureaucratic impossibility of tracking when a taxpayer may one day utilize a tax attribute previously subject to the GAAR. Also, the GAAR loses a significant part of its bite if taxpayers can use aggressive tax planning to create tax attributes knowing that they will suffer no actual punitive financial consequences were they to lose a GAAR challenge.

To remedy this, the Budget proposes to rewrite the definitions of “tax benefit” and “tax consequences” in section 245 of the Act. The amended definition of “tax benefit” will include a reduction, increase or preservation of an amount that could at a subsequent time be relevant for or result in a reduction of tax or an increase in a refund of tax. This will catch abusive tax avoidance transactions that create, increase, or preserve tax attributes such as PUC, adjusted cost base, CDA, loss carry overs, general rate income pool, refundable dividend tax on hand, amongst many others.

The unsavory part about this proposed amendment is that the amendment has retroactive effect. This amendment will apply to transactions carried out in the past, as long as the Minister has not already issued a GAAR notice of determination before the April 7, 2022, Budget Date.

The Government isn’t done tinkering with the GAAR though. The Government in its 2020 Fall Economic Statement announced that it was going to take steps to “strengthen and modernize Canada’s general anti-avoidance rule (GAAR) rules”. In this Budget, the Government informs that they are going to make good on this promise, and that they will be issuing a consultation paper on GAAR, followed by a consultation period during the summer of 2022, and subsequently issue legislative proposals to be tabled by end of 2022. As we have stated in the past, we are not against reforming the GAAR, but given the Canadian government’s track record with tinkering anti-avoidance rules, we are likely to end up with an overly broad GAAR that becomes an albatross to ordinary commercial transactions. These changes continue a trend that when the the government is unhappy with precedent, they may legislate it away, constantly keeping tax practitioners and taxpayers on their toes.

A Commitment to Create a New Minimum Tax Regime for “High Earners”

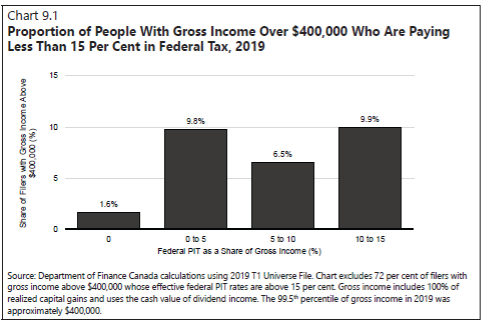

In the Budget documents, the government announced that they are committed to examining a “new minimum tax regime” that will “go further towards ensuring that all wealthy Canadian pay their fair share of tax”. To justify this, the government pointed out that 28% of taxpayers with gross income above $400,000 pay an average federal personal income tax of 15% or less, “due to significant use of deductions and tax credits”. They produced the following graph to illustrate their point:

Wow, that sounds outrageous. We should grab our pitchforks now…On a closer reading, however, this is really misleading and irresponsible rhetoric.

First, the government is citing only federal personal income tax, which makes the tax burden sound lower than it is. Pretty much everyone in Canada, even the “wealthy”, paying federal income tax also pays provincial income tax. Secondly, the fine print in the chart states that percentage is calculated on gross income which includes 100% of realized capital gains. In our experience, many taxpayers who have a spike in their income level in a year is often due to capital gains realized in the year, e.g., selling a rental property or selling a business. Capital gains are only 50% includable in income. The top federal tax bracket in Canada is 33%, so half of that is 16.5%. 15% federal income tax suddenly doesn’t sound very low compared to 16.5% does it?

Thirdly, this statistic ignores the fact that the tax system calculates tax using a progressive tax rate for different bands of income. Someone whose income is at the top 33% federal bracket [>$220K] also has their income taxed at the lower progressive rates as well. Below we have calculated how much federal personal income tax is due for someone earning $400,000 of different types of gross income, with no special credits or deductions:

|

Type of income – $400,000 |

Estimated federal income tax |

Effective tax rate |

|

Employment income |

$109,000 |

27.3% |

|

Non-eligible dividend income |

$87,700 |

21.9% |

|

Eligible dividend income |

$76,700 |

19.1% |

|

Capital gain |

$43,900 |

11.0% |

It is likely that most of the people cited by the government to have paid less than 15% are those who recognized significant capital gains in the year. And if that’s what the government finds offensive, then perhaps they should just increase the capital gains inclusion rate (which obviously we hope they do not) rather than tinkering with a new minimum tax regime. Furthermore, there are tax-exempt capital gains as well, such as on qualified small business corporation shares, which further skews this statistic.

There are many other legitimate reasons why someone’s tax payable could be significantly lower than their “gross income” would otherwise suggests. Common examples are charitable donations, spousal support payments, interest expense on investment loans, high medical expenses, and loss carryovers. We would like to believe none of these should be offensive from a policy perspective. It is also unclear whether gross income ignores expenses incurred to earn business, rental, or other property income.

Finally, even for regular employment income, at $400,000, the effective federal tax rate is just 27.3%, which is indeed quite a bit higher than 15% but it is not the wide gulf that the rhetoric is making it sound like.

Enough ranting. What can we speculate about the new minimum tax system that the government says they will release details on in the 2022 fall economic and fiscal update? Keep in mind there already is an existing alternative minimum tax regime which applies when income with preferential treatment arises (e.g., when the lifetime capital gain exemption is claimed on the sale of qualified small business corporation shares). The government could tinker with the existing regime and increase the amount of alternative minimum tax when such preferential treatment is claimed. Additionally, the government could perhaps cause alternative minimum tax to arise when an individual claims too much interest and financing expenses, claims foreign tax credits on foreign sourced income, or donation tax credits (although there already are various legislative limits on donations).

For now, all we can do is stay tuned on this topic.

Additional Taxes on Large Financial Institutions

Budget 2022 proposes to introduce two additional taxes on large financial institutions:

- A one-time 15% tax on bank and life insurer groups on its taxable income that exceeds $1B.This one-time tax would apply for affected taxpayers for taxation years ending in 2021. The resulting liability would be imposed for the 2022 taxation year and would be payable in equal amounts over five years. This additional one-time tax is being coined as the Canada Recovery Dividend. In our opinion, the name for this one-time tax is cutesy and borderline offensive.

- An additional 1.5% tax on the taxable income of bank and life insurer groups on profits more than $100M for taxation years that end after April 7, 2022.

In our opinion, the introduction of these additional taxes is offensive. Some quick comments:

- The additional taxes will, no doubt, be passed through to Canadians in some form or fashion.In other words, the affected financial institutions will not simply accept these new taxes without trying to preserve their overall profit margins and returns to shareholders;

- Will the financial institutions respond to the increased taxes by increasing interest rates on certain loans to consumers, increased or additional fees, or increased premiums on life insurance or other products? If so, Canadian consumers will be the ones that ultimately pay the price;

- Many Canadians hold Canadian bank and life insurance stocks in their portfolios, or such stocks are held in their pension funds that they are a beneficiary of.Will their pension funds or other holdings’ yields be negatively affected by possible reduced distributions by the affected financial institutions? If so, again, it will be average Canadians that will be negatively impacted.

- We are overall concerned that the issues (as we understand have been raised by many financial institutions about this possible tax to government) have fallen on deaf ears.

- If the government feels comfortable targeting certain “wealthy” sectors, what affected industry will be next?Will the oil and gas sector be next targeted, for example, as a result of high oil and gas prices? This is a dangerous precedent.

- The government continues the trend of believing they are the best party to decide where spending should exist, rather than working with private industry in targeting investments or programs.

Employee Ownership Trusts

In the 2021 federal budget, the government announced that it would “engage with stakeholders to examine what barriers exist to the creation of [employee ownership trusts]”. Apparently, the consultations revealed that the main barrier to the creation of employee ownership trusts in Canada was the lack of a dedicated trust vehicle under the Income Tax Act. Accordingly, the government announced that it would indeed create a dedicated trust vehicle – the Employee Ownership Trust – to support employee ownership. Further consultations will apparently take place to assess further details. This is somewhat interesting but ultimately the lack of detail makes this proposal difficult to assess and comment further.

Government to Review the SR&ED Program

The Scientific Research and Experimental Development (SR&ED) Program is a program that has long utilized tax incentives to encourage Canadian businesses of all sizes and in all sectors to conduct research and development (R&D) in Canada. Corporations, individuals, trusts, and members of a partnership can access the SR&ED program and benefit from the tax incentives that it provides.

These SR&ED tax incentives come in three forms: an income tax deduction, an investment tax credit (ITC), and, in certain circumstances, a refund. All are based upon a system that will provide a benefit that ranges from 15% to 35% of the eligible expenditures incurred in the course of conducting qualifying SR&ED activities.

The SR&ED Program successfully provides more than $3 billion in tax incentives to over 20,000 eligible applicants annually, making it the single largest federal program that supports business R&D in Canada.

According to the Budget material, the government intends to undertake a review of the program, first to ensure that it is effective in encouraging R&D that benefits Canada, and second to explore opportunities to modernize and simplify it. Specifically, the review will examine whether changes to eligibility criteria would be warranted to ensure adequacy of support and improve overall program efficiency.

Historically, changes to the SR&ED program have reflected restrictive measures to limit the amount of the benefit received by the applicant and to also limit the flexibility associated with the filing deadlines for those entities wishing to apply for the program. We anticipate that the intention of the review will be to further tighten the eligibility requirements for the program and may also revisit the applicable rates for benefits awarded to eligible recipients.

As part of this review, the government will also consider whether the tax system can play a role in encouraging the development and retention of intellectual property stemming from R&D conducted in Canada. In particular, the government will consider, and seek views on, the suitability of adopting a patent box[1] regime to meet these objectives.

From a policy perspective, it remains extremely important that Canada continues to have a robust mechanism for the purpose of supporting SR&ED activities in Canada. SR&ED tax incentives not only help claimants, but they also better society by encouraging innovation, technological advancements, and the pursuit of scientific and technological knowledge, discoveries and ideas that may lead to Canadian economic growth and improved competitiveness.

More Money for CRA

Despite throwing reams of cash at the CRA in recent years, a recent report from the Parliamentary Budget Officer has revealed that the CRA remains somewhere between “meh” and “yuck” when it comes to key performance indicators when compared to international counterparts. The report from the PBO states that “In most cases, Canada is never quite far from the average, usually performing marginally better or marginally worse than the comparable countries.”[2] This does not reflect particularly well on the CRA, despite funding commitments between 2016 and 2026 that total in excess of $3 billion, with nearly $2 billion targeted specifically for compliance activities.

Budget 2022 continues the theme of “throwing more cash at the problem” as the government proposes to provide an additional $1.2 billion over five years, starting in 2022-23, for the CRA to expand audits of larger entities and non-residents engaged in aggressive tax planning; increase both the investigation and prosecution of those engaged in criminal tax evasion; and to expand its educational outreach.

The budget documents suggest that these measures are expected to recover $3.4 billion in revenues over five years, with additional benefits to be realized by provinces and territories whose tax revenues will also increase as a result of these initiatives.

In his report, the PBO recommends that “…as the government considers the provision of additional funding into the Agency, parliamentarians should continue to pay attention to its performance and outcome.”[3] With additional funds flowing to the CRA with each federal budget announced, it is important we all continue to keep an eye on the performance and outcomes of the Agency.

GST/HST on Assignment Sales by Individuals

Generally, an assignment sale of a residence is a transaction in which a purchaser (an “assignor”) under an agreement of purchase and sale with a builder of a new home sells their rights and obligations under the agreement to another person (an “assignee”)

The current indirect taxation of an assignment sale depends on the details of the transaction. If the primary purpose was to resell the interest in the agreement, then the sale would be subject to GST/HST, however, if the there was another primary purpose, such as to use the property as a residence, then the sale would be exempt from GST/HST. Budget 2022 proposes to make all assignment sales subject to indirect tax. The ambit of this proposed change is to increase the certainty of the GST/HST implications of an assignment sale, it appears that this certainty comes with a cost regardless of if circumstances for an individual change.

New “Boutique Tax Credits”

In 2015, the CBC decried the then-Harper Conservative government for the introduction of an array of boutique tax credits. The government was “scolded” for targeted tax-reduction for segments of the electorate rather than focusing simply on an across-the-board tax reduction. Well, apparently the current Liberal government believes that this “boutique” approach to tax reduction continues to play well with Canadians and has dropped a variety of tax “goodies” on Canadians with the introduction of Budget 2022. Here is a sampling…

Tax-Free First Home Savings Account (FHSA)

- New registered account to help individuals save for their first home;

- Contributions to an FHSA would be deductible and income earned in an FHSA would not be subject to tax;

- Qualifying withdrawals from an FHSA made to purchase a first home would be non-taxable;

- The government will release its proposals for other design elements in the near future.

Home Buyers’ Tax Credit (HBTC)

- Budget 2022 proposes to double the HBTC amount to $10,000;

- Provide up to $1,500 in tax relief to eligible home buyers;

- Spouses or common-law partners would continue to be able to split the value of the credit as long as the combined total does not exceed $1,500 in tax relief;

- This measure would apply to acquisitions of a qualifying home made on or after January 1, 2022.

Multigenerational Home Renovation Tax Credit

- The proposed refundable credit would provide recognition of eligible expenses for a qualifying renovation;

- A qualifying renovation would be one that creates a secondary dwelling unit to permit an eligible person (a senior or a person with a disability) to live with a qualifying relation;

- The value of the credit would be 15 per cent of the lesser of eligible expenses and $50,000;

- This measure would apply for the 2023 and subsequent taxation years, in respect of work performed and paid for and/or goods acquired on or after January 1, 2023.

Home Accessibility Tax Credit

- A non-refundable tax credit that provides recognition of eligible home renovation or alteration expenses in respect of an eligible dwelling of a qualifying individual;

- A qualifying individual is an individual who is eligible to claim the Disability Tax Credit at any time in a tax year, or an individual who is 65 years of age or older at the end of a tax year;

- The value of the credit is calculated by applying the lowest personal income tax rate (15 per cent in 2022) to an amount that is the lesser of eligible expenses and $10,000;

- Budget 2022 proposes to increase the annual expense limit of the Home Accessibility Tax Credit to $20,000 Budget 2022 proposes to increase the annual expense limit of the Home Accessibility Tax Credit to $20,000;

- This measure would apply to expenses incurred in the 2022 and subsequent taxation years.

Labour Mobility Deduction for Tradespeople

- Temporary relocations to obtain employment may not qualify for existing tax recognition for moving or travel expenses;

- Budget 2022 proposes to introduce a Labour Mobility Deduction for Tradespeople to recognize certain travel and relocation expenses of workers in the construction industry, for whom such relocations are relatively common;

- This measure would allow eligible workers to deduct up to $4,000 in eligible expenses per year;

- Specific definitions and restrictions as to “eligible individual”, “eligible temporary relocation” and “eligible expenses”;

- Restrictions on amounts claimed for supporting payments received by an employer;

- This measure would apply to the 2022 and subsequent taxation years.

This is a high-level sampling of some of the more interesting additions to the list of boutique tax credits available under the Income Tax Act. As always, the question becomes, how has the introduction of this vast array of tax credits supported the simplification of the Income Tax Act? We have reached a point in time where the Act now must be published in two printed volumes and has become an unwieldy behemoth of legislation. However, it seems that the government of the day believes it is important to have “a little something for everyone” in Budget 2022.

[1] A “patent box” is a special very low corporate tax regime used by several countries to incentivize research and development by taxing patent revenues differently from other commercial revenues. It is also known as intellectual property box regime, innovation box or IP box.

[2] “International Comparison of the Canada Revenue Agency’s Performance” Office of the Parliamentary Budget Officer, Ottawa, Canada; March 29, 2022; pg.3

[3] Ibid; pg.4

Related Blogs

Have you ever wondered how much your US citizenship is costing you? Why renouncing could save you hundreds of thousands and open new doors for financial opportunities.

As US expats prepare for another expensive and stressful tax filing season, we’ve compiled a list of...

Looking to make 2024 your last filing year for US taxes? Here’s what you need to do.

In a recent survey, one in five US expats (20%) is considering or planning to renounce their...

Travelling to the US? If you’re a US expat who doesn’t renounce properly, your trip may never get off the ground.

Air travel can be stressful. Rising airfares and hotel costs, flight cancellations, pilot strikes, long security wait...