Blog + News

October 9, 2020 Announcement on CEWS Extension, CEBA Expansion and Help for Commercial Tenants

[My colleague, Kim Moody, and I recorded an episode of the podcast about the October 9, 2020 announcement. You can listen to it here.]

As part of the September 23, 2020 Throne Speech, the Government announced its intention to extend the CEWS program to summer of 2021. Under the current CEWS legislation, the amount of CEWS phases out over the remaining months of 2020, so an extension to next summer surely meant the Government had to revisit these mechanics. Not surprisingly, that is what the Government announced one day before the beginning of the Canadian Thanksgiving long weekend in its October 9, 2020 announcement. The announcement also contains other goodies: expansion of CEBA and a new Canada Emergency Rent Subsidy (CERS). Details are lacking on all of these, but below is a quick summary to get you up-to-speed.

Freezing of CEWS Base Percentage

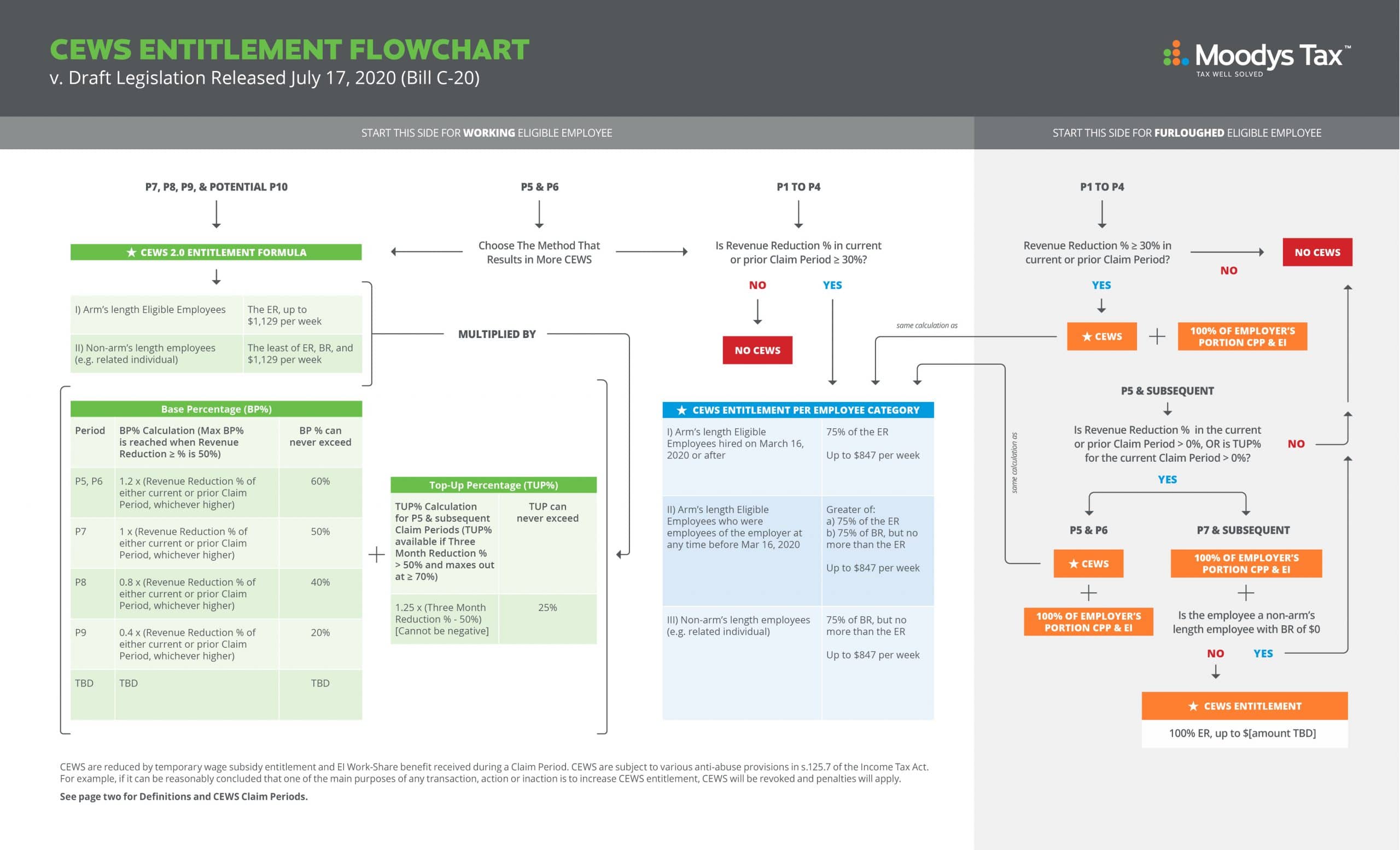

Currently, Canada is in its 8th CEWS Claim Period which calculates CEWS using a “Base Percentage” that is 0.8 of the Revenue Reduction Percentage up to 50%, and a “Top-Up Percentage” that is 1.25 of the Revenue Reduction Percentage in excess of 50%. The maximum CEWS amount is generally reached when a business’ revenue decline is 70% or more. Here are two brief numeric illustrations:

Example #1: 20% revenue reduction percentage, and 20% top-up revenue reduction percentage.

CEWS = wages in respect of a week up to $1,129 x [(Base Percentage: 0.8 x 20%) + (Top-Up Percentage: 0% since top-up revenue reduction percentage did not exceed 50%)]. This results in $180.64 of CEWS for the week.

Example #2: 70% revenue reduction percentage, and 70% top-up revenue reduction percentage.

CEWS = wages in respect of a week up to $1,129 x [(Base Percentage 0.8 x 50%) + (Top-Up Percentage: 1.25 x (70% – 50%))]. This results in $733.85 of CEWS for the week, or in other words, 65% of the $1,129 maximum wage threshold.

For a more fulsome depiction of the CEWS mechanics that currently exists, please refer to our Firm’s flowchart.

{kind=link}

The Base Percentage computation was slated to decrease to 0.4 of the revenue reduction percentage, starting October 25, 2020. This would have reduced the maximum CEWS entitlement (available on a 70% revenue decline or more) from 65% to 45%. According to the Government in its October 9, 2020 news release, this reduction will not occur:

“The subsidy would remain at the current subsidy rate of up to a maximum of 65 per cent of eligible wages until December 19, 2020.”

The Government also announced that the CEWS regime will be extended until June 2021. This is certainly great news for employers across the country.

The CEWS legislation in the Income Tax Act will need to be amended to affect this since the CEWS phase out was hardcoded into the CEWS legislation. We do not anticipate the Liberal Government will have trouble getting the amendment passed since they obtained the NDP’s support of the initiatives in their Throne Speech. The new legislation will certainly contain some sort of phasing out of the CEWS amount during the months of 2021, and it will be interesting to see what further complications and anti-abuse provisions the Government may add to this next version of CEWS legislation.

Expansion of CEBA

As part of the September 23, 2020 Throne Speech, the Government promised an expansion of the CEBA program. Currently, the CEBA provides a $40,000 interest-free loan to eligible businesses, of which 25% will be forgivable provided the business repays 75% of its maximum loan balance by December 31, 2022. Under the expanded program, an eligible business can access an additional $20,000 of CEBA loan, and half of that $20,000 will be forgiven if the loan is repaid by December 31, 2022. The deadline to apply for CEBA will also be extended to December 31, 2020.

We are still waiting for further details to be released on the expanded CEBA program. Hopefully, the Government will also revisit the qualification criteria for CEBA as there are currently some unfairness and arbitrariness in terms of who qualifies. For example, businesses that resale products can treat materials consumed to produce that product as “eligible non-deferrable expense(s)” to qualify for CEBA, whereas businesses in the service industry cannot claim their input expenses in a similar manner (e.g. truck drivers and their cost of gas).

New Canada Emergency Rent Subsidy (CERS) Program

The current business rent subsidy program is the Canada Emergency Commercial Rent Assistance (CECRA) and it has been in place since April of this year. However, in our experience, the take up of this program was dismal as it requires a commercial landlord to rely on their tenants’ assertion of their revenue decline percentage and to pre-emptively agree on a net decrease in rental revenue. As a result, many businesses who are barely hanging on are not getting any relief in respect of occupancy expenses.

The Government appears to recognize this and is introducing a new Canada Emergency Rent Subsidy (CERS) program that appears will deliver subsidy directly to the business tenant (rather than just to the commercial landlord as under the CECRA program). No details have been released, but the Government mentioned the following parameters:

- The rent subsidy would be provided directly to tenants, while also providing support to property owners. The new rent subsidy would support businesses, charities, and non-profits that have suffered a revenue drop, by subsidizing a percentage of their expenses, on a sliding scale, up to a maximum of 65 per cent of eligible expenses until December 19, 2020. Organizations would be able to make claims retroactively for the period that began September 27 and ends October 24, 2020.

- A top-up Canada Emergency Rent Subsidy of 25 per cent for organizations temporarily shut down by a mandatory public health order issued by a qualifying public health authority, in addition to the 65 per cent subsidy.

Since the Government already designed a sophisticated system for measuring revenue decline, and many businesses are already keeping track of monthly revenue declines for their CEWS claims, using the same to administer the CERS appear to be a logical choice. Although the devil is in the details, this will hopefully give some much-needed relief to businesses across the country.

All of the above is certainly good news for businesses and can hopefully stem widespread permanent financial ruin for many Canadian entrepreneurs. Long term, it remains to be seen how the tremendous cost of these programs, accompanied by eye-popping and out-of-control government budgetary deficits, will come back to bite all of us.

Related Blogs

Have you ever wondered how much your US citizenship is costing you? Why renouncing could save you hundreds of thousands and open new doors for financial opportunities.

As US expats prepare for another expensive and stressful tax filing season, we’ve compiled a list of...

Looking to make 2024 your last filing year for US taxes? Here’s what you need to do.

In a recent survey, one in five US expats (20%) is considering or planning to renounce their...

Travelling to the US? If you’re a US expat who doesn’t renounce properly, your trip may never get off the ground.

Air travel can be stressful. Rising airfares and hotel costs, flight cancellations, pilot strikes, long security wait...