Blog + News

Proposed Canadian “income sprinkling” rules V2: not many feathers, lots of hissing

1. Executive Summary

On December 13, 2017, the tax and business community finally got the chance to review version two of the tax on split income (“TOSI”) or the so-called “income sprinkling” proposals. The Department of Finance originally announced that these revised proposals would be released later this fall. That would make this release two weeks early (if one subscribes to the astronomical definition of the seasons rather than the meteorological, which would have defined fall to end on November 30), but is the revised proposal a gift or a lump of coal?

After briefly reviewing these proposals, we are disappointed. Yes, major overhaul has been done to remove some of the most problematic issues of the originally proposed TOSI rules, many of which were brought to the government’s attention through the 51-page joint committee submission in which our firm has been actively involved. However, the fact that a “reasonableness” test and substantial complexity still exists is disheartening due to the uncertainty and difficulty they will create for taxpayers in applying the rules and the Canada Revenue Agency (CRA) and the Courts enforcing them.

We also believe that income splitting should be permitted between spouses (not just for private business income, but for all types of income) since we do not think it’s fair or appropriate for tax policy to ignore indirect contributions of one spouse to the success of the other. In our view, a much better approach in addressing the government’s perceived abuse would have been to adopt a bright-line age-24 test whereby the TOSI applies to all individuals age 24 and under (with limited exclusions for special circumstances), and to no one over that age threshold. This approach would probably prevent the most egregious situations that the government is offended by and would have caused the least disruption to Canadian private businesses. V2 of the TOSI rules missed the opportunity to provide simple and objective rules to address the perceived mischief. Disappointing.

Louis XIV’s finance minister, Jean-Baptiste Colbert, said “The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing.” Sadly, the various tax changes by our government over the last two years (e.g. subsection 55(2), small business deduction changes, work-in-progress rules for professionals) have strayed significantly from this principle.

2. A Technical Review of V2 of the TOSI Proposals – December 13, 2017

For the technically inclined, the balance of this blog will be of interest. If you’re not technically inclined, suffice it to say that the rules are complex and you can stop here and get specialist advice before advising on future income splitting.

In V2, the government was able to reduce the applicable draft legislation from 15 pages to 11. Although there have been noticeable simplifications—the circularity of the July 18, 2017 proposed legislation has been minimized and replaced by introducing more definitions, for instance—there still remains significant convolutedness. Unfortunately, the current (and much more sensible) “kiddie tax rules” remain a mere shadow of the new proposed rules. Some say you cannot argue with progress, but that definitely was not us.

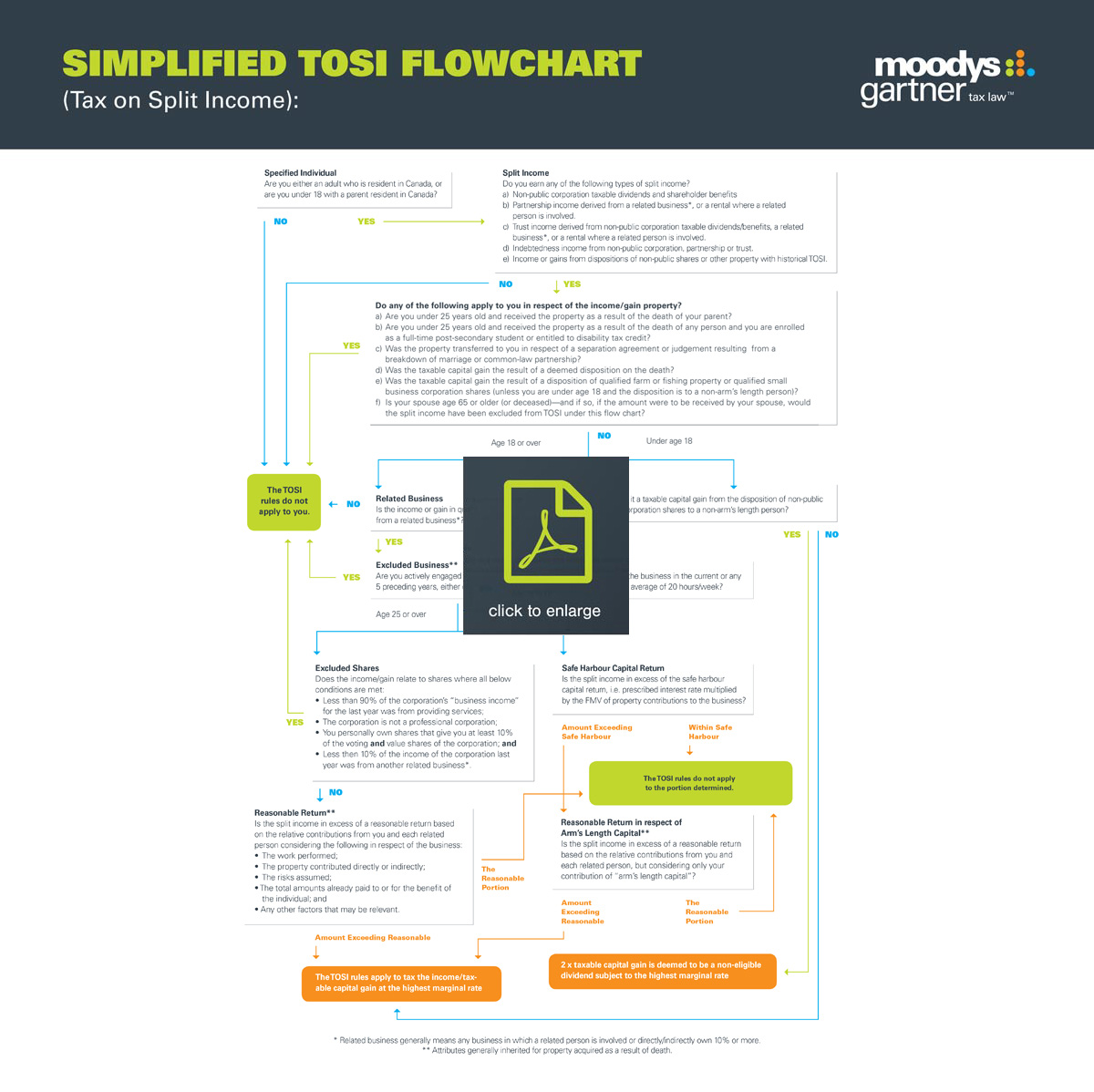

Put simply, the TOSI rules apply the highest marginal rate of personal tax to income that is “split income” received by a “specified individual” and that is not an “excluded amount.”

December 13, 2017 changes to the definition of “specified individual”

Where the proposals from July 18 seriously convoluted the definition of a “specified individual” by including reference and connection to income from the business, the version from December 13 simplified and broadened the definition to generally include any adult individual who is a resident in Canada, or any minor whose parent is a resident in Canada.

December 13 changes to the definition of “split Income”

Under the July 18 proposed TOSI rules, the definition of split income was expanded to include income from indebtedness, income or capital gains from the disposition of property, income from a conferred benefit and secondary income earned on income previously subject to the attribution rules or TOSI rules. The December 13 proposed legislation has taken a middle-ground approach by retaining the indebtedness income and income or capital gains from the disposition of property, while dropping the latter two additions from July 18. The table below summarizes the current definition as compared to the July 18 proposed definition of split income and again compared to the December 13 proposed definition.

|

Current Definition |

July 18 Proposed Definition |

December 13 Proposed Definition |

|

(a) Unlisted dividends and shareholder benefits |

(a) Unlisted dividends and shareholder benefits |

(a) Unlisted dividends and shareholder benefits |

|

(b) Partnership income |

(b) Partnership income |

(b) Partnership income |

|

(c) Trust income |

(c) Trust income |

(c) Trust income |

|

|

(d) Indebtedness income |

(d) Indebtedness income |

|

|

(e) Income or gains from dispositions of property |

(e) Income or gains from dispositions of property |

|

|

(f) Income from conferred benefit; and |

(f) – income from conferred benefit; and |

|

|

(g) Secondary income |

(g) – secondary income |

December 13 changes to the definition of “Excluded Amount”

The definition of “excluded amount” has been greatly expanded from the July 18 version to include income resulting from:

- Property transferred in respect of a separation agreement in the context of a breakdown of a marriage or common-law partnership;

- A taxable capital gain that results on the deemed disposition as a result of the death of a taxpayer; and

- A taxable capital gain from the disposition of qualified farm or fishing property or qualified small business corporation shares;

These additions are certainly welcomed, and, particularly the expansion to relationship breakdown and death, are necessary to prevent unfair tax results arising from dispositions that are entirely involuntary.

The previous references in the July 18 version to “split portion” and the reasonableness test contained therein has been removed. Instead, analogous concepts have been imported into the “excluded amount” definition directly through a number of new defined terms: “excluded business,” “excluded shares,” “safe harbor capital return” and “reasonable return.” The easiest way to explain how the “excluded amount” definition applies in practice is to break the rules down as to how they apply to each of the following four age categories:

i. under age 18;

ii. age 18 to 24; or

iii. age 25 and over, unless the individual’s spouse who is the primary business contributor has reached the age of 65; and

iv. spouse is age 65 and older.

i) Under age 18

Any income described in the definition of split income received by a minor (unless from certain inherited property) is subject to the TOSI. The existing kiddie tax rules remain with virtually no changes, other than the inclusion of indebtedness income and income or capital gains from the disposition of property as described above.

ii) Age 18 to 24

Income described in the definition of split income received by an individual that has reached the age of 17 but not the age of 24 before the year is subject to the TOSI rules unless the amount received is considered to fall into one of five exclusions.

Firstly, there is an exception of certain inherited properties similar to minors. Secondly, if the income in question is not derived directly or indirectly from a “related business,” it is not subject to the TOSI rules. For example, Mr. A owns and operates a corporation and the corporation declares and pays a dividend to his 18-year-old daughter. Because of Mr. A’s relation to his daughter, the dividend income is considered to be from a “related business” and would be subject to the TOSI rules unless it falls into another exclusion. Alternatively, if Mr. A’s daughter receives dividends from a corporation in which no related person is actively engaged or is a 10 per cent (or more) owner, she would not be deriving income from a “related business” and TOSI should not apply to her. The July 18 proposal extended the meaning of related persons to uncles, aunts, nieces and nephews—this change has been abandoned in the December 13 proposal.

Thirdly, income derived directly or indirectly from an “excluded business” is excluded from the TOSI rules application. An “excluded business” is considered to include a business in which the individual is actively engaged on a regular, continuous and substantial basis in either the taxation year in question, or any five historical years. Whether an individual meets this actively engaged threshold appears to be a factual test, but in an attempt at a bright-line test, the government enacted a deeming rule whereby one is deemed to have met the actively engaged threshold by working in the business at least an average of 20 hours per week during the portion of the year in which the business is operational.

Certainly, it will be ideal to be able to rely on the 20-hour test rather than trying to substantiate that one has engaged on a regular, continuous and substantial basis, but this will presumably require increased efforts in the form of record keeping tracking hours worked (timesheets for everyone! Yay!) Perhaps the most interesting aspect of the “excluded business” rule is that once an individual has met the actively engaged test for five years, which do not need to be consecutive, then the individual (and anyone inheriting the individual’s interest) will forever be protected by the “excluded business” exclusion. This is probably what the government meant when they touted that someone who made a “meaningful contribution” will not be subject to TOSI

Therefore, if Mr. A’s daughter averaged at least 20 hours per week of work in the business operated by Mr. A’s corporation from 2014 through 2018, Mr. A can pay his daughter any amount of dividend every year starting from 2014 and for the entire lifetime of the daughter without TOSI applying to the daughter (to the extent she is 18 or over in 2014).[1]

If the individual between age 18 to 24 derives income from a “related business” and has not worked for a sufficient amount of time in the business to qualify under the “excluded business,” the only possible way for the individual in this age category to avoid or reduce the TOSI is if capital has been contributed into the business. There are two alternative capital contribution tests for these individuals: the “safe harbour capital return” test and the “arm’s length capital / reasonable return” test.

The “safe harbour capital return” test reduces the income includable in TOSI by a notional amount calculated by the prescribed rate of interest multiplied by the fair market value (“FMV”) of property contributed by the individual in support of the related business. It is important to note that the computation of safe harbour capital return does not require a carve-out of capital obtained from a non-arm’s length source, but the prescribed rate of interest is a low rate (currently 1%). Therefore, if Mr. A’s daughter (between age 18 to 24) has contributed $100,000 to Mr. A’s corporation either as debt or equity (irrespective of how she obtained the $100,000) and Mr. A’s daughter does not work in the business, she will be allowed $1,000 of income per year before TOSI starts applying, under the current prescribed rate of interest.

Alternatively, an individual in this age category is entitled a “reasonable return” test based only on the individual’s “arm’s length capital.” Therefore, the amount subject to TOSI can be reduced or eliminated if the individual is able to justify that the amount received represents a reasonable return on his or her own property contributed to the business, meaning that the property is neither transferred to him or her by any means from a related person, derived from a related business, nor borrowed from any source.

iii) Age 25 and over

The rules are less stringent for individuals who have attained the age of 24 before the year. Just like the 18 to 24 age group, an individual who has attained age 24 before the year will not be subject to TOSI if the income is not derived directly or indirectly from a “related business” or if the income is derived from an “excluded business.” In addition to this, individuals in this age group will not be subject to TOSI on income from “excluded shares.”

“Excluded shares” are defined to mean shares of a corporation owned by the individual where:

- Less than 90% of its “business income” for the last tax year that ends at or before that time was from the provision of services;

- The corporation is not a professional corporation;

- Immediately before that time, the individual owns shares representing at least 10% of the votes and FMV of the corporation;

- All or substantially all of the income of the corporation’s income for the last tax year that ends at or before that time is not derived directly or indirectly from another related business, e.g. collecting rent from a related business.

At first glance the “excluded shares” exclusion appears to be generous for adult individuals who are not professionals and who own 10% or more of a corporation, allowing them unlimited opportunity to income split. Many typical private corporations are held 50/50 by spouses or common-law partners, thus each shareholder would hold more than 10% of votes and value. However, there are a number of potential issues that could arise that make this “excluded shares” exclusion to become unavailable. We will discuss some of these issues in more detail below.

In the event the individual deriving income from a related business cannot fit under the excluded business or the excluded shares definition, the individual could still qualify for the “reasonable return” exclusion. Unlike the reasonable return test for those between age 18 to 24 which limits the determination to only capital contribution, the reasonable return test for individuals age 25 and over considers an array of factors, assessed based on relative contributions of the individual and each related person:

- The work performed by the individual;

- The property contributed directly or indirectly by the individual (but, as stated above, could only consider “arm’s length capital” for this age group);

- The risks assumed by the individual in respect of the business;

- The total amounts already paid to or for the benefit of the individual in respect of the business; and

- Any other factors that may be relevant.

This reasonable test is a resurrection of the July 18 reasonableness test, but there are a number of interesting differences and observations worth pointing out. Like the July 18 version of the proposed rule, there is uncertainty whether historical contribution of work / property contributed / risk assumed can be considered in the reasonableness test. It is possible to interpret the provision to mean that one can only look at current year contributions. On the other hand, practical challenges abound if a business owner needs to tally all historical amounts already paid to him or her since inception of the business in order to arrive at what is reasonable in the current year. It is disappointing that the government did not take the opportunity to clarify this in the legislation.[1]

An interesting addition to the test is that “any other facts that may be relevant.” This could be used to address situations where profits are not tied directly to work / property contributed / risk assumed, e.g. windfall gains. On the flip side, this could be used by the CRA to reduce the reasonable amount an individual is otherwise entitled to if it feels there are “other factors” present that justify such a reduction. Time will tell how this discretion will be applied.

Perhaps the most interesting, though, is that this revised reasonableness test no longer refers to an arm’s length standard. Instead, the test focuses on the relative contribution of each related persons. Of course, it is still a subjective and potentially difficult exercise to measure and compare the contribution of each person to a business, but at least there appears to no longer be a requirement to benchmark a business owner’s return against an arm’s length standard which the July 18 version would have required.

iv) Individual with a spouse who is 65 and up

In an attempt to align with the existing pension income-splitting rules, the TOSI rules will not apply to income received by an individual from a related business if the individual’s spouse or common-law partner has attained the age of 64 before the year and the amount would have been an excluded amount were it to be included in her or his income. In other words, income splitting from a private business will generally be allowed starting in the year a contributing spouse turns 65.

TOSI Rules on Capital Gains

Subsections 120.4(4) and (5) are currently in place to re-characterize an otherwise capital gain into a non-eligible taxable dividend under certain non-arm’s length dispositions. The July 18 proposals expanded the application from minor shareholders to also include adults, resulting in very adverse tax consequences in many unexpected situations. In the latest version, subsections (4) and (5) has been narrowed back to only being applicable to minors. The business and tax community can breathe a collective sigh of relief at least on this front.

Under the December 13 proposal, TOSI will not apply to capital gain on disposition of qualified farm or fishing property (QFP) or qualified small business corporation (QSBC) shares, regardless of the age of the holder or whether the lifetime capital gain exemption (LCGE) is claimed. This means that capital gain splitting with non-active family members and multiplication of the LCGE will still be allowed for shares and property that qualify (although non arm’s length disposition of QSBC shares by minors will still be re-characterized as a non-eligible dividend). Capital gains on shares or property that do not qualify will be subject to the same TOSI rules and exclusions described earlier. Regularly purifying private corporations to maintain QSBC share status will likely be a more prominent tax planning strategy going forward as a result.

Effective Date

Proposed rules still apply for 2018 and subsequent years, i.e. 2017 is the last year under the current TOSI regime. However, it is worth noting that for taxpayers seeking to rely on the “excluded shares” exclusion, they will have until the end of 2018 to meet the condition of owning at least 10% of the outstanding shares of a corporation in terms of votes and value. Notwithstanding, it is disappointing that the Government did not delay the application of these proposals to January 1, 2019. As mentioned, the proposals are very complex and it will certainly take the tax and business community quite some time to digest and properly apply. Affected taxpayers deserve more time to appropriately understand and properly plan their affairs.

Problems with the “Excluded Shares” Exclusion

i. Carve-out for professional corporation and service businesses

It’s no surprise that the government would deny the benefit of the “excluded shares” exclusion to professional corporations given its rhetoric over the last two years against professionals, especially doctors. A professional whose spouse or common-law partner also owns shares in the professional corporation will not be able to rely on this exclusion to income split, because of the explicit carve-out of professional corporation in the definition of “excluded shares.” The spouse or common-law partner will have to rely on other exclusions, such as working over 20 hours per week in order to qualify for the “excluded business” exception.

What is surprising is that the government is denying this exclusion to any and all businesses who derive their income from the provision of services. The policy rationale behind this is presumably that the government does not want businesses that are ‘professional-like’ to be able to enjoy the exclusion.

However, to discriminate against all service business in one broad stroke is analogous to shooting mice with an elephant gun, especially given that a large majority of Canadian businesses are service-oriented.[2] For example, a couple who starts a hair salon as 50/50 shareholders will not be able to income split if one spouse does not contribute to the business; whereas another couple who starts a hotdog stand as 50/50 shareholders will be able to income split regardless of contribution. Both businesses could have similar capital requirements and risk profile, but the tax treatment is vastly different simply because one couple went into the service industry and the other decides to sell products.

This also affects large family-owned service businesses, such as construction service companies, oilfield services companies, etc. We believe this is a very unfair approach that unnecessarily punishes the majority of privately-owned businesses, and we believe that proper enforcement of the current personal services business rules would have been sufficient to address most of the government’s concerns.

ii. All or substantially all of the income not derived from another “related business”

Another part of the definition of “excluded shares” that appears problematic is the requirement that all or substantially all of the income of the corporation not be derived directly or indirectly from another “related business.” Assume a typical Holdco-Opco structure where Holdco shares are owned 50/50 by husband and wife. Opco’s business would be a related business to both husband and wife because each them indirectly owns 10% or more of Opco. This would mean that Holdco shares can probably never be “excluded shares” because its income is indeed derived directly or indirectly from another “related business.” Hopefully this is an unintended technical glitch because we see no policy rationale as to why a private business owner should be punished simply because a multi-tier holding structure is chosen, which often is done for important business reasons. However, what is the likelihood of the government fixing this glitch retroactively effective January 1, 2018? One would hope so since the one year transitional period for “excluded shares” only apply in respect of the 10% holding requirement.

iii. What is “business income?”

One more aspect of the “excluded shares” exclusion that is sure to result in uncertainty and controversy is that one of its key conditions is based on the concept of “business income.” “Business income” is not a term that has been used elsewhere in the Act. On the one hand, there has always been a distinction between income from property and income from business, and the courts have generally distinguished between the two by considering the level of services, the number and value of transactions, the time devoted to the activity, etc. On the other hand, a “business” is broadly defined in subsection 248(1), and includes an “undertaking of any kind whatever.”

So, what is “business income?” This will be an important distinction, for example, for a holding corporation whose sole activity is to make investments. Is the income from such investments “business income” or not? If not, the shares of the corporation could potentially be “excluded shares” for any family shareholder owning 10% or more, thus allowing income splitting regardless of contribution.

iv. Is the new “Excluded Shares” Definition a Disguised Attack on Family Trusts?

The requirement of 10% votes and value explicitly refers to shares that are owned by an individual. A common holding structure for private corporations is to hold the shares in family trusts. When the private corporation pays a dividend to the family trust, the trust often distributes that dividend to a beneficiary of the trust. Similarly, if the family trust disposes of the shares of the private corporation, the trust may distribute the taxable capital gain to a beneficiary. Although subsections 104(19), (21) and (21.2) of the Act allow the trust to make designations to deem a beneficiary to have received the respective dividend or taxable capital gain, and even deem the beneficiary to have disposed of the shares in question, the Act does not deem the beneficiary to hold or own the private corporation shares held by the trust. Because of this, it is possible that beneficiaries of a family trust would never be able to rely on the “excluded shares” exclusion for dividends or taxable capital gains allocated from a trust. Is this an intentional result by the government? Possibly.

Recall that the July 18 proposal denied the claiming of LCGE of any property held in trust but the government announced in October 2017 that they had abandoned those proposals. This is perhaps an alternative way to curb income and capital gain splitting through trusts. Nevertheless, even if the “excluded shares” exclusion is unavailable, an individual disposing of properties that are not QSBC or QFP property could still potentially avoid TOSI by meeting the “excluded business” or “reasonable return” exclusions with sufficient contributions.

3. Concluding Comments

Phew! All we have done here is only a preliminary overview of the December 13 TOSI proposals. There are likely many more issues and technical glitches in the legislation that tax geeks like us will stumble across in the coming weeks. By the government’s own account, these TOSI measures will generate approximately $200 million of additional tax revenue per year—a drop in the bucket for the government’s budget. Yet, the administrative and documentation burden for Canadian private businesses will be enormous, particularly when coupled with the corporate passive income proposal that the government is committed to introducing.

Finally, as has been common with our existing government, a gender-based analysis commentary is included as part of the TOSI proposals:

Data show that men represent over 70% of higher-income earners initiating income sprinkling strategies, and women represent about 68% of recipients of sprinkled dividends (and 58% of recipients of income derived from trust and partnerships). While this income is of benefit for recipients, it also creates incentives that reduce female participation in the workforce. Increased participation of women in the workforce is a source of economic opportunity for individuals and is a major driver of overall economic growth.

We had to read the above twice to make sure the government was serious when they produced such commentary. Really? This statement is shocking especially to members of our firm who have children and stay-at-home spouses. Without exception, the decision for members of our firm who have stay-at-home spouses was made for the betterment of the family as a whole with tax impacts not at all being part of the analysis for the resulting decision. To suggest that the income-sprinkling proposals will contribute to incentives for stay-at-home females to enter the workforce is nonsensical and offensive (notwithstanding that the authors are not economists and have not studied gender-based issues but instead rely on real life and common sense).

For a little bit of feathers, there will a lot of hissing indeed.

[1] The CRA guidance released on the same day as the December 13, 2017 proposals alluded to past contributions, but CRA guidance is not binding and not necessarily evidence of Parliament’s intention behind the proposed legislation.

[2] This relieving rule is actually prejudicial against new entrepreneurs. Owners of established private businesses who are able to substantiate five years of active engagement will be able to income split for the rest of their lives, and when these owners pass away, their descendants inheriting their interest will also be entitled to receive income without TOSI applying again for the rest of their lives. Contrast this to a family starting out a new business in 2018, having to start the 5-year clock and having to cope with the TOSI rules.

[3] June 2016 statistics from the Government of Canada website states that “of all employer businesses, 916,527 (78.5 %) operate in the service-producing sector, compared with 251,451 (21.5%) in the goods-producing sector.” https://www.ic.gc.ca/eic/site/061.nsf/eng/h_03018.html

Related Blogs

Have you ever wondered how much your US citizenship is costing you? Why renouncing could save you hundreds of thousands and open new doors for financial opportunities.

As US expats prepare for another expensive and stressful tax filing season, we’ve compiled a list of...

Looking to make 2024 your last filing year for US taxes? Here’s what you need to do.

In a recent survey, one in five US expats (20%) is considering or planning to renounce their...

Travelling to the US? If you’re a US expat who doesn’t renounce properly, your trip may never get off the ground.

Air travel can be stressful. Rising airfares and hotel costs, flight cancellations, pilot strikes, long security wait...